Quick Take: What are the top institutions that offer student loans in the Philippines?

The Landbank i-STUDY Program offers up to PHP300,000 with a 5% fixed interest rate p.a. To explore more options, you can check out various scholarships on Edukasyon.ph . You can also get Tonik Credit Builder Loan so you can start building your credit at the same time! Download the Tonik App to apply.

Are you considering pursuing higher education but worried about the cost? You're not alone, luv! With rising inflation, it’s getting more and more expensive to get that undergraduate degree. That’s why many students and their families turn to financial aid to help cover the expenses. One of the most popular ways of funding higher education in the Philippines is through student loans.

But with so many options available, how do you choose the right one?

In this article, we’ll explore the different types of student loans in the Philippines and provide tips on how to choose and manage your student loans effectively.

Table of Contents

- What are Student Loans?

- Student Loan Options in the Philippines

- The Role of a Co-signer in Securing Student Loans

- Interest Calculation for Student Loans: What You Need to Know

- How to Choose the Right Student Loan

- Managing Your Student Loan in the Philippines

- Understanding the Consequences of Default

- Strategies for Loan Consolidation

- Conclusion

Did You Know: Good Credit Unlocks Better Loans

Bad credit gets you bad loans. Good thing it's never too late to start building with Tonik Credit Builder Loan!

What are Student Loans?

Student loans are a type of financial aid that helps students cover the cost of their education. They are designed to assist students and their families in financing higher education expenses, such as tuition, other fees, books, gadgets, and living expenses.

When considering financial aid options, it's important to understand the differences between student loans and other forms of financial assistance. Here is a brief comparison:

| Type | Features |

| Scholarships |

|

| Grants |

|

| Student Loans |

|

Student Loan Options in the Philippines

When it comes to student loans in the Philippines, there are several options available for students and parents alike. These options can be categorized into the following:

Government Program

The government offers various loan programs to help students finance their education through student loans in the Philippines. These programs often have favorable terms and conditions. Here are three options you can choose from:

| Loan | Key Features | Eligibility Requirements |

| CHED UniFAST Student Loan Program |

|

|

| Landbank i-STUDY Program |

|

|

| SSS Educational Assistance Loan Program |

|

|

| GSIS Educational Loan |

|

|

Private Banks and Financial Institutions

Private banks and financial institutions also offer student loans in the Philippines. Banks usually do not award loans based on an applicant’s needs. Rather, they have a set of eligibility requirements that determine whether or not they will approve your loan.

While they usually have higher interest rates and additional fees and charges, student loans from Philippine banks also offer flexible repayment options that could work best for your situation. Here are some example of student loans in the Philippines offered by banks and other financial institutions:

| Loan | Key Features | Eligibility Requirements |

| Tonik Loans |

|

|

| BPI SIP Loan for School |

|

|

| InvestEd Student Loan |

|

|

| Bukas Tuition Installment Plan |

|

|

Educational Institutions

Some schools and universities in the Philippines offer their own loan programs to assist students in financing their education. These programs may have specific eligibility requirements and application processes. It's important to check with individual institutions for more information.

| Loan | Key Features | Eligibility Requirements |

| UP Short-term Cash Loan |

|

|

| De La Salle University Student Loan Program |

|

|

| Mapua University Student Financial Assistance Program |

|

|

The Role of a Co-signer in Securing Student Loans

Embarking on the journey of higher education is thrilling, yet the path of securing financial aid can seem daunting, particularly when it comes to fulfilling the stringent eligibility criteria for student loans. This is where the invaluable role of a co-signer comes into play. A co-signer is someone, typically a parent, guardian, or close family friend, who agrees to share the responsibility of your student loan. They commit to repaying the loan if the primary borrower fails to do so, providing lenders with an added layer of security.

Incorporating a co-signer into your loan application can significantly bolster your chances of approval, especially for students with limited credit history or insufficient income. By presenting a co-signer with a strong credit background, lenders might be more inclined to offer favorable loan terms, including lower interest rates and higher loan amounts. However, it’s crucial to approach this arrangement with clarity and mutual understanding, acknowledging the potential risks and responsibilities it entails for both the student and the co-signer.

TOCInterest Calculation for Student Loans: What You Need to Know

Navigating through the world of student loans can be daunting, especially when it comes to understanding how interest affects your repayments. Just like choosing the right course can set the stage for your future career, understanding interest calculation is crucial in managing your financial future effectively.

- The Basics of Interest Calculation: Interest on student loans in the Philippines is calculated based on the principal amount — the total sum borrowed. This interest can be fixed or variable, significantly impacting your overall repayment amount. Fixed interest rates remain constant throughout the life of the loan, offering predictability in your monthly payments. Variable rates, however, can fluctuate based on market conditions, potentially increasing or decreasing your repayment amount over time.

- How It Impacts Your Loan: Interest calculation plays a pivotal role in determining how much you'll end up paying back. For instance, a loan with a 6% annual interest rate will incur interest costs at that percentage of the outstanding principal balance each year.

- Compounding Interest: Some student loans compound interest, meaning the interest itself earns interest over time. This can significantly increase the total amount you owe. It's important to ask your lender how interest is compounded on your loan to anticipate how it may grow throughout your education and beyond.

Interest calculation on student loans is not just a minor detail; it’s a critical factor that affects how manageable your loan will be in the long run. By understanding how interest is calculated and applied to your loan, you can make smarter borrowing decisions, aligning your educational aspirations with your financial realities.

Before committing to a student loan, use loan calculators available online to simulate your loan repayment scenarios based on different interest rates and repayment terms. This step can provide a clearer picture of your future financial commitments and help you plan accordingly.

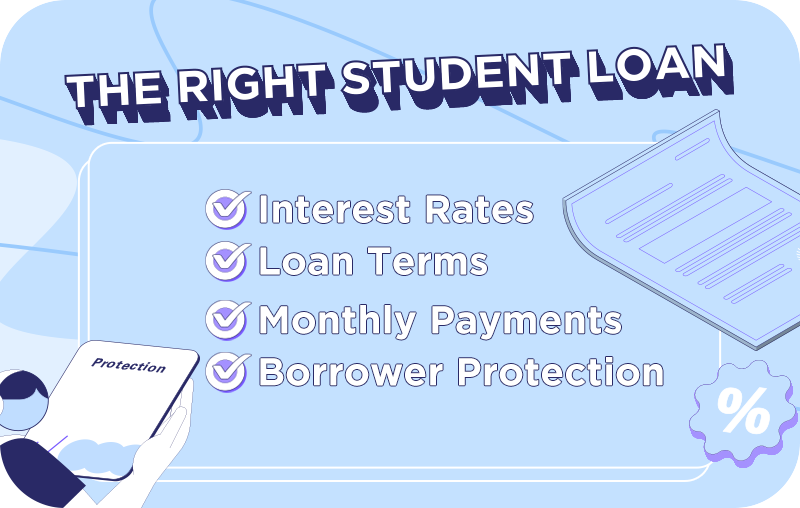

TOCHow to Choose the Right Student Loan

Choosing the right student loan in the Philippines is an important decision that can have long-term financial implications. Here are some factors to consider when selecting a student loan:

-

Interest Rates: Compare the interest rates offered by different lenders. Remember: Lower interest rates can save you money in the long run, hun!

-

Loan Terms: Consider the length of the loan term and the repayment options available. Longer loan terms may result in lower monthly payments but can also mean paying more in interest over time.

-

Monthly Payments: Calculate the estimated monthly payments for each loan option. Make sure the payments are manageable within your budget.

Borrower Protections: Look for loans that offer borrower protections such as deferment, forbearance, and loan forgiveness options. These protections can provide flexibility in case of financial difficulties.

Managing Your Student Loan in the Philippines

Once you have chosen a student loan, it's important to learn how to manage it effectively. Here are just a few ways you can do it:

-

✓Borrow Only What You Need: It may be tempting to borrow a huge loan amount, especially if you’re eligible for it. But this is something we don’t recommend, luv. Borrow only what you need to cover your education expenses. This will help you avoid unnecessary debt and make repayment more manageable.

-

✓Triple Check Your Lender: Before taking out a student loan, make sure your lender is legit. Be wary of lenders that offer loans that are too good to be true! They could most likely be scams!

-

✓Make Timely Payments: Pay your monthly loan installments on time to avoid late fees and penalties. Consider setting up automatic payments to ensure you never miss a payment. Automatic debit can also sometimes qualify you for a small interest rate reduction.

-

✓Create a Budget: Develop a budget that includes your loan payments. Allocate funds specifically for loan repayment and prioritize them in your budget. This will help you stay on track and ensure you have enough money to cover your monthly payments.

-

✓Pay During Grace Period: If possible, start making payments on your student loans during the grace period or while you're still in school. This can help reduce the amount of interest that accrues and gets added to your principal balance.

-

✓Consolidate Your Loans: Consolidating multiple student loans into one payment can help you simplify repayment. It can also potentially lower your monthly payments by extending the repayment term.

Understanding the Consequences of Default

Defaulting on a student loan can have serious financial consequences for borrowers. Some of the consequences of default include:

-

Collection fees

-

Wage garnishment or salary deductions

-

Damage to credit scores

- Ineligibility for other loans or financial aid programs

It's important to understand the consequences of default and take steps to avoid it. If you are struggling to make payments, consider reaching out to your lender to discuss alternative repayment options.

Suggested Read: The Process of Debt Collection for Unpaid Cash Loans in the Philippines

TOCStrategies for Loan Consolidation

Consolidating your student loans can be a helpful strategy for managing your debt. Here are some strategies you must keep in mind:

-

Make a List of Your Loans: Start by making a list of your current loans and credit cards. Include the total balance, interest rate, minimum monthly payment, and total remaining payments. This will help you determine which loans to consolidate and which to keep separate.

-

Compare Options: There are several options for consolidating your loans, including personal loans, home equity loans, balance transfer credit cards, and debt management programs. Research and compare the pros and cons of each option to determine which one is best for you.

-

Consider Interest Rates: One of the primary benefits of consolidating your loans is potentially lowering your interest rate. Look for loans with lower interest rates than your current loans to save money over time.

- Avoid New Debt: Consolidating your loans won't be effective if you continue to accumulate new debt, luv! Avoid using credit cards or taking out new loans while you're repaying your consolidated loan.

Remember, consolidating your loans may not be the best option for everyone. It's important to consider the pros and cons and consult with a financial advisor or loan counselor before deciding.

TOCOne Final Note, Luv

Pursuing higher education can be expensive, but student loans can help make it more accessible. By understanding the different types of student loans in the Philippines and following these tips for choosing and managing your student loan, you can successfully pay off your debt and achieve your educational goals. Don't let financial concerns hold you back from pursuing your dreams. But also, don’t forget to loan responsibly, luv!

Share this post

Most Popular