Quick Take: What makes a good credit score in the Philippines?

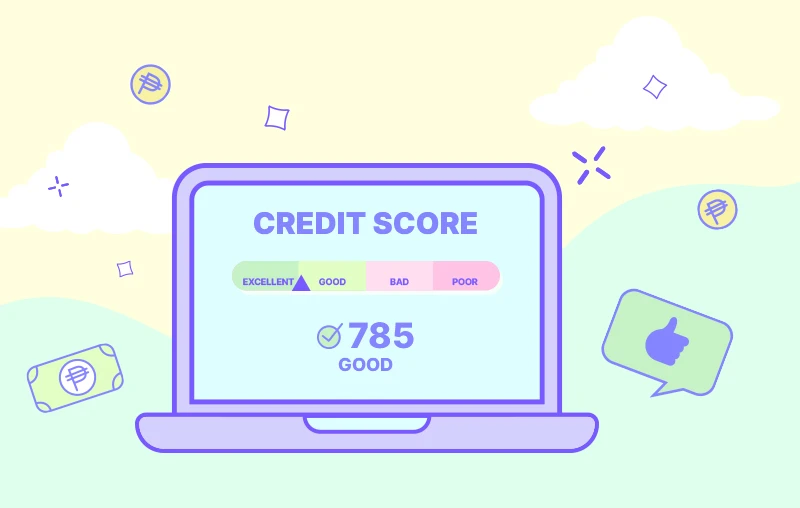

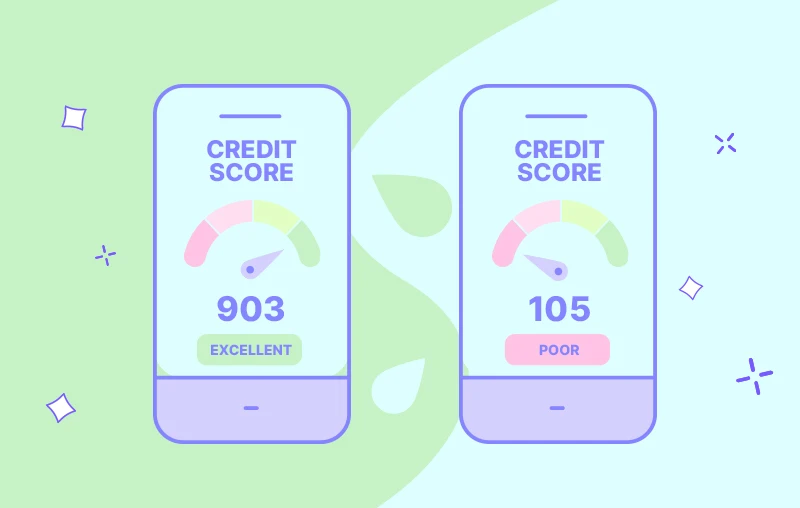

Credit scores in the Philippines range from 300 to 850, with 850 being the best. A score between 700-759 is considered good, 650-699 is fair, and 600-649 is poor. Scores below 600 are classified as bad.

Learn all about how credit scoring works in the Philippines and how Tonik is pushing boundaries with its new products!

Picture this: you’re super excited about a shiny new gadget you want to buy! A new laptop, perhaps, to help you work better? While you don’t have enough funds for it, you think, hey, I can always take out a small loan so I can pay for it! So, you apply to a financial institution that can lend you some money for a loan, like a bank maybe! You’ve got everything covered—you seem to have all the criteria down, including a stable job and regular salary.

Expectation then meets reality: The bank responds that they can’t get you the loan at this time. What could’ve caused them to decline it? Everything on your end seems to be alright.

This is where credit scores come in. You might have heard about credit scores while navigating your way through banking as well as your finances. It may seem like a harmless number on the get-go, but it actually holds a lot of power, especially when you’re looking at getting a loan, a credit card, or other similar credit accounts. You might be clueless about it too.

Let’s go all in about the truth about credit scoring in the Philippines, what it is exactly, and what you need to think of when trying to raise your credit score. We’ll also be sharing some other financial alternatives that don’t need credit scores or history, too! So come in with an open mind and read on right here, luvs.

Table of Contents

- Credit scores—what are they anyway?

- How Your Credit Score Influences Loan Terms Through Risk-Based Pricing

- What number makes a good credit score?

- What are the components or factors of a credit score?

- I need to keep my credit score HIGH! You got any tips on how to do that?

- Wait a minute...all of this sounds a little complex. So, if I don't have any history with previous banks, credit cards, and loans, I won’t have a credit score?

- Oh, really?! If I don’t have a credit score and barely any history with banks, how can I get a loan or similar credit accounts?

Tired of High-Interest Loans?

A solid credit history can unlock better loan terms. Start building with Tonik Credit Builder Loan!

Credit scores—what are they anyway?

A credit score is more than just a simple number, hun—think of it like your rating. On Uber, you can rate drivers, but drivers can rate you too based on how you are as a passenger. Credit scores are kind of like that! This number is the score that you’ve got based on your ability to manage financial obligations and debt, like paying your loans back or your credit card dues. Financial institutions like banks and credit companies use your credit score to decide on your access to loans, credit, and other financial services. In a nutshell: if you have a good credit score, then you can get these financial services a lot easier compared to when you have a bad one. So it’s great to keep this credit score high so that your chances of your loan and credit application approval would be equally high as well!

Right here in the Philippines, credit scoring is handled by the Credit Information Corporation, or the CIC for short! So far, it is the only centralized registry of credit data in the country. How it works is that companies like insurance firms, telecom companies, and banks give their customers’ credit history to the CIC. The CIC will then collect the information and turn this into coherent credit reports.

TOC- Table FIndHow Your Credit Score Influences Loan Terms Through Risk-Based Pricing

Understanding your credit score is just the start. It's also vital to grasp how lenders use this score to apply risk-based pricing to loans and credit accounts. This means the better your credit score, the more favorable the terms you might receive—like lower interest rates or more flexible repayment options.

In essence, a high credit score can signal to lenders that you're a low-risk borrower, potentially unlocking better financial terms. This system underscores why maintaining a good credit score is crucial not just for approval, but for securing the most advantageous terms on the loans and credit lines available to you.

TOC- Table FInd

What number makes a good credit score?

Credit scores in the Philippines range from 300-850. 850 is the highest and means you have the BEST credit score! However, around the 700-759 range is already a pretty good number to have! On the other hand, the 650-699 range is a fair score to have, and 600-649 is poor. Anything that scores below 600 means that it’s a bad credit score.

TOC- Table FIndWhat are the components or factors of a credit score?

When improving your credit score, you’ve got to consider these 5 factors that it’s based on.

- Payment history – This is the most obvious factor, based on how responsible you are with payments and how regularly/on time you pay your debts. Did you know that if you miss a payment cycle, your credit score can drop by 90 to 100 points? Yikes!

- Length of credit history – This is based on how long you’ve had credit cards or loan accounts. Got credit cards? The age will be averaged according to your oldest card, newest card, as well as all the other cards you have in your wallet.

- Credit types used – Got a mix of different credit accounts such as cash loans, car loans, credit cards, mortgage, etc.? Lenders may look at this to check on how you’re able to manage all of these accounts.

- Amount owed – This is the total amount of the money you currently owe across all your credit accounts, including credit cards. The bigger the amount of money you owe or the more debt, you aren’t likely to get approved for more loans or credit accounts.

- New credit applications – This refers to all your new applications to credit cards, loans, and the like. If you’re applying for multiple credit accounts at the same time, your score could be affected, so be wary about that!

I need to keep my credit score HIGH! You got any tips on how to do that?

All you need to do is organize your finances and be super responsible with them!

- Build a good credit score as early as possible. Got a credit card at a young age? Use that opportunity to go by the rules.

- Pay your dues (credit, bills, etc.) either early or on time. It goes on your record if you keep missing payments. If it’s possible, make your payments automatic and use the features of your online banking apps.

- Only spend within your credit limits! Keep track of how much you use your credit and don’t overspend, or else you’ll be flagged!

- As much as possible, don’t apply for credit cards and loans one after the other.

- Settle all credit and loans before even thinking of getting new ones.

- Learn how to strategize and space out your loan applications accordingly.

- Lastly, monitor your credit score to keep track of your progress. You can learn how to check your credit score in the Philippines here.

It’s a big responsibility, so make sure you do it the right way! Another tip is to have a budget so you can track your expenses, bills, etc. and manage to save at the same time! Read up on budgeting and money management apps here.

Wait a minute...all of this sounds a little complex. So, if I don't have any history with previous banks, credit cards, and loans, I won’t have a credit score?

Yes, luv! To have a credit score, you need to have a history of previous credit accounts, from cards to loans. Companies also look at your bank transactions and history. These are the things that’ll allow lenders or banks to gauge your financial responsibility. But don’t fret! There have been loads of innovative fintech institutions nowadays that can get you loans or credit accounts without all those things. Which then leads us to your next question, most likely...

TOC- Table FIndOh, really?! If I don’t have a credit score and barely any history with banks, how can I get a loan or similar credit accounts?

Don’t stress! You’re not alone! Did you know? Only 47.1% of Filipino adults have borrowed money as of April 2023 and as much as 80% of Filipinos don’t have credit history! You’ll get there eventually though, especially now that more and more digital banks are popping up that will make getting a bank account and debit/credit cards so much easier than before! The Bangko Sentral ng Pilipinas (BSP) is consistently looking for solutions that’ll make the country more financially inclusive and let Filipinos access better financial services.

One of them, of course, is Tonik! Apart from it being an all-digital bank that was also first to be issued a digital banking license by the BSP, wherein you can open an account from your phone in just minutes, it also has innovative products that are changing the game everywhere! Need a loan but have no credit score and no pre-existing bank account with another bank? No problemo, luv!

The Tonik Credit Builder Loan is an easy solution to your financial woes, and you can borrow up to PHP20,000 without credit score! Yes, say goodbye to borrowing from your friends, family, or elsewhere! But how is this even possible?

Tonik relies on world-class alternative credit scoring technologies for credit decisions. All you need to submit is your monthly income and current profession (self-employed included). After a final verification call with you, the credit decision is made within minutes through proprietary AI-driven underwriting. In a nutshell, yup, it’s all thanks to technology, baby! No more long, manual checks that’ll take forever. The times are changing, so we’ve got to have our products and financial services adapt as well, right?

So take a baby step with our Credit Builder Loan that allows you to take a huge leap into financial freedom. Eventually, we can build your credit score together. Just remember the tips above!

We got you if ever you need a (quick) loan! Check out our page on our available loans right here to find out how you can apply for the one that’s right for you.